Duration of inventory turnover in days. Inventory turnover ratio

Inventory turnaround time is the time in days it takes for inventory to be sold. The duration of the turnover of stocks shows the rate of transformation of stocks from material into monetary form.

The analysis of the duration of the turnover of stocks is carried out in the FinEkAnalysis program in the Business Activity Analysis block.

Inventory Turnover Formula

Inventory Turnover Time = Days in Period / Inventory Turnover Ratio

The shorter the duration of inventory turnover, the less funds are tied up in this least liquid group of assets. The recommended values of the indicator depend on the industry. The decrease in the indicator is a favorable trend.

Synonyms

inventory holding period, inventory turnover period, inventory turnover period

Was the page helpful?

More found about the duration of the turnover of stocks

- Analysis of the turnover of current assets in the agricultural and baking sectors of the economy If average annual cost inventories in 2015 compared to 2011 increased by 161.6%, the increase in the value of current assets was equal to 190%, then revenue increased by 120.6% Duration one inventory turnover in 2015 compared to 2011 increased from 13

- Development of a method for calculating the average duration of stay of the working capital of an enterprise in the analyzed period duration inventory turnover at production costs a accounts receivable- by revenue and then

- Methodology for the analysis of current assets of a commercial organization Tz average turnover in days duration one turnover of stocks SPR - the cost of goods sold products works services Zsr - average

- Factors and problems of efficient use of current assets in the agricultural sector Inventory turnover ratio 22.3 1.8 1.6 Duration one inventory turnover days 16,207,226 Accounts receivable turnover ratio 4.6 10.1 12.0

- Analysis of financial statements. Practical analysis based on accounting (financial) statements Amount of used stocks thousand rubles 15701 18772 22910 20152 18776 3 Duration inventory turnover days 365 x p 1 p 2 183 209 207 278 355

- Analysis and evaluation of the effectiveness of the financial policy of the organization Internal audit efficiency of resource use which can be built on the basis of determining the following indicators of the inventory turnover ratio duration turnover of the ratio of the purchase price to the average market price of the presence of a shortage or excess of stocks 8.

- Study of the influence of the duration of the operating and financial cycles on the financial stability of enterprises in the Tula region duration operating cycle is influenced by four factors the value of the period of turnover of stocks of raw materials and components

- The role of business analysis in the organization's accounts payable management system duration operating cycle for 54 days then

- Comprehensive analysis of the financial condition of an educational organization Inventory turnover turnover p 9 p 5 79.57 92.70 13.13 116.5 17 Duration turnover of inventories days 360 p 16 5 4 -1 80.0 Table 15. Profitability

- Development of a methodology for calculating the average turnover period of an enterprise's inventory in work in progress management accounting identify factors that affect duration the average period of inventory turnover and identify reserves for its reduction Introduction Working capital turnover

- Planning of current production assets of the enterprise Work in progress in days is duration turnover of funds in production or the rate of working capital stock in WIP Work in progress in

- Analysis of the financial condition in dynamics Turnover ratio of material assets 0.439 0.511 3.994 2.93 3.495 3.056 Duration turnover shelf life days 820 705 90 123 103 -717

- Analysis of receivables of a commercial organization Such an enterprise is relatively liquid in a dynamic sense - it can produce products, sell it, accumulate it cash from buyers and all in a relatively short period of time It does not depend to the same extent on static liquidity factors ... An analysis of the operating cycle based on inventory turnover ratios of inventories in days and receivables turnover in days helps to give an overall assessment

- The role of financial analysis in assessing the business activity of an enterprise In turn, the inventory turnover ratio increased by 2.42 turnovers in the reporting year, thereby decreasing duration one inventory turnover for 29 days which is a positive trend List of sources used 1.

- Inventory turnaround time Analysis business activity How duration Inventory turnover period Inventory turnover time formula Inventory turnover time Duration of one period

- Methods for assessing the risk of bankruptcy of enterprises The first includes indicators indicating possible difficulties and the likelihood of financial instability of the organization in the near future recurring significant losses in the main activity expressed in a chronic decline in production reduction in sales and constant unprofitability low values of liquidity ratios and a tendency to decrease the presence of chronic overdue accounts payable and receivable increase to dangerous limits of the share of borrowed capital in its total amount deficit of own working capital systematic increase duration capital turnover excess stocks of raw materials and finished products use of new sources of financial resources for

- Analysis of the use of capital General duration working capital turnover days 84.293 69.732 -14.561 including in - stocks 52.299

- A multi-criteria approach to the analysis of entrepreneurial risks This indicates an increase in the independence of the functioning of the organization and the ability to timely necessary formation of reserves Probability of entrepreneurial risks LLC Kuban - low The autonomy coefficient in 2013 increased by... 7.018 4.967 -2.024 -2.051 b Duration turnover - accounts receivable 79 49 44 -35 -5 - accounts payable 52 52

- Topical issues and modern experience in analyzing the financial condition of organizations - part 4 In the second direction, indicators of the efficiency of the use of material labor and financial resources are determined labor productivity capital productivity turnover of inventories duration of the operating cycle, the turnover of advanced capital Traditionally, in the analysis of business activity, indicators of asset turnover are used ... Traditionally, in the analysis of business activity, indicators of asset turnover, including inventories and receivables of own funds, as well as the turnover of accounts payable, are used. These indicators are calculated in ... These indicators are calculated in turnover times by comparing the indicators of the average balances of the estimated indicators and their turnovers for the period from

- Indicators of business activity of Elan-95 LLC Average period of turnover of receivables days 18.2 17.6 6.1 4.3 9.3 20.6 21.8 10.5 5.7 Average period... Average period of turnover accounts payable days 84.1 97 58.1 58.3 52.9 33.7 15.1 29.7 26.1 Duration production cycle average inventory turnover period days 35.4 38.4 44.3 43.5 40.4 41.3 36.1

Update of the article from 07/17/2019.

When analyzing the company's activities, we recommend looking not only at the turnover of goods, but also to evaluate it together with the level of service. If the assortment of the company is quite diverse, then we recommend analyzing the turnover in monetary terms, and not in kind, since the cost of goods can differ by hundreds and even thousands of times.

When calculating the turnover in monetary terms, it is necessary to fix prices on the first or last day of the analyzed period. Otherwise, due to price changes, turnover may increase, which will not reflect the real picture.

In some companies, turnover is calculated in times a year. In this case, the higher the score, the better. In other companies, turnover is calculated in days. This indicator is called "coverage in days". In this case, the smaller it is, the better."

One of the main performance indicators commercial enterprise- inventory turnover. The turnover ratio (or inventory) is the ratio of a company's sales to its assets. This indicator makes it clear how quickly the stock in the warehouse is sold. Inventory turnover ratio can be used to understand how efficiently and successfully a company uses its assets to generate income.

Calculation of inventory turnover in natural units.

To calculate the turnover of goods in natural units, you must:

1) Select a period (week, month, year)

WhereТЗ1, ТЗ2, ... ТЗn - the value of the inventory on certain dates of the analyzed period,

inventory turnover formula

How to calculate the turnover ratio?

Weekly sales and inventory data:

Sales per period = 3+5+6+3+2+5+2 = 26 units

How to calculate the turnover ratio for a group of goods?

For a group of goods, the turnover calculation logic represents the following sequence of actions:

- Period selection

- Calculation of the amount of sales for a group of goods

- Calculate the amount of balances for a group of goods for each day

- Calculate average inventory

- Calculate turnover ratio

|

∑ Remains |

|||||||

|

∑ Sales |

|||||||

Sales for the period = 30+33+48=111 units

Calculation of the cash turnover ratio

- Select period (week, month, year)

- Calculate the average inventory for the selected period in monetary units (can be calculated using individual product or by product group)

where ТЗ1, ТЗ2, ... ТЗn - the value of the commodity stock on certain dates of the analyzed period,

J - the purchase price of the goods

n is the number of dates in the period.

![]()

Tsr - selling price

The formula for calculating the turnover of funds:

Turnover \u003d Pd.e. / Tzav d.u.

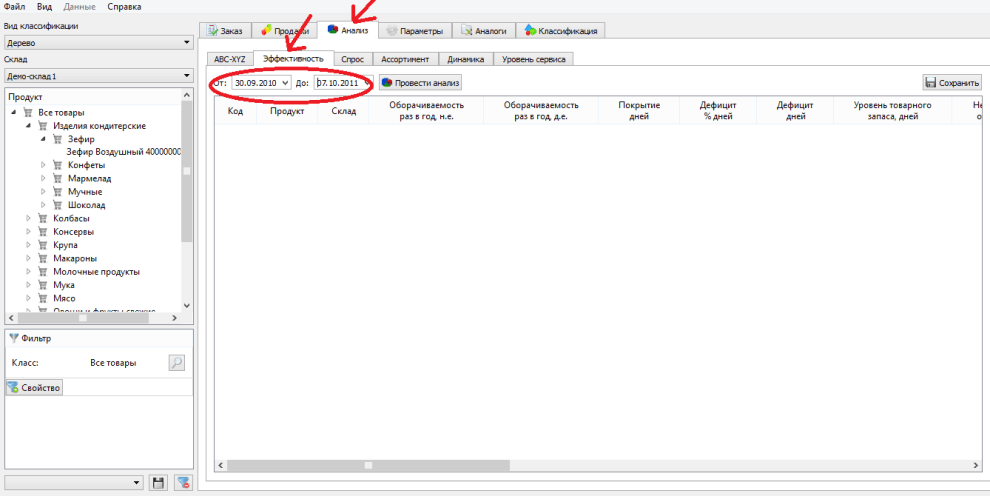

Inventory Turnover Calculation in Forecast NOW!

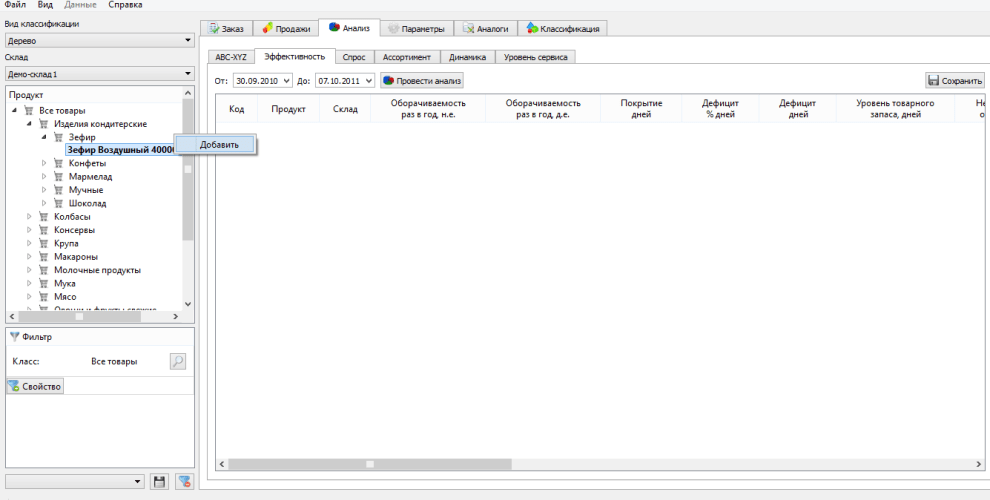

In the Forecast NOW! It is possible to calculate the inventory turnover ratio for the year in two clicks, both in monetary and natural units:

1. Go to the "Analysis - efficiency" tab and set the period for which you want to calculate the turnover:

2. Right-click or double-click on the product or product group for which you want to calculate the turnover

3. Click "analyze" and you will see the turnover ratio for the selected period:

Under such a term as inventory turnover, it is customary to understand a parameter that characterizes the renewal of stocks of any product, goods, raw materials, materials during a certain billing period. If we talk about the warehouse complex, then in this case the turnover parameter determines the speed at which goods are produced and released from the warehouse. It is this parameter that determines the degree of efficiency with which two services interact - the purchasing service and the sales service.

If the turnover parameter is low, this clearly indicates an unsatisfactory indicator of financial and commercial activities companies. In addition, it serves as a signal that the company has an excess of cargo, or that the company has poor sales.

And vice versa, if the turnover parameter is high, the faster the turnover of finances invested in goods is carried out, and, consequently, the return of money in the form of revenue occurs faster. In other words, for the successful commercial activity of the company, it is necessary to observe the optimality of stocks, and it is recommended to constantly monitor such a parameter as inventory turnover.

In order to constantly monitor inventory turnover, you need to know the following indicators:

- a measure of the average stock of goods for a particular period. Those. you need to know how much cargo, goods or raw materials are in the warehouse complex, for example, within a month;

- duration of the billing period. Any time interval can be used in this capacity, for example, a year, a month, for perishable goods - a week;

- turnover rate for billing period. This parameter is calculated in warehouse prices.

Now a little more about these indicators. The indicator of the average stock of goods is calculated as the sum at the beginning of the period and at its end, divided in half. If the calculation of the indicator of the average stock of goods is carried out, then it is necessary to use the formula of the average chronological number, and not the arithmetic average.

What is measured and how is inventory turnover calculated?

In the case when we are talking about the inventory turnover parameter, as a rule, the following indicators are used:

- inventory turnover ratio. This parameter is calculated as the ratio of the cost goods sold to the amount of stocks for the billing period on average;

- inventory turnover rate in days. It determines how many days the average warehouse stock will be sold. The formula for calculating the inventory turnover indicator in days is as follows: About days \u003d Average stock of goods * number of days / Turnover of goods for this period;

- the indicator of inventory turnover of goods in times. Shows how many times during the billing period the product was able to "turn around", i.e. be realized.

The formula for calculating the inventory turnover ratio in times is as follows:

Time = Cost of goods sold / Average stock of goods for the period.

Inventory turnover does not have approved or generally accepted normative indicators. The most optimal figures should be determined as a result of analysis within the same industry.

Inventory turnover calculator

To achieve a greater effect, it is recommended to conduct such an analysis within each specific enterprise. In addition, it should be remembered that for companies that are inherent in high profitability, as a rule, a lower rate of inventory turnover is characteristic in comparison with companies with a lower rate of return.

inventory turnover (inventory turnover) shows how many times during the period under review the company used the available average inventory balance. The indicator characterizes the quality of the company's stocks, the efficiency of their management, allows you to identify the remains of unused, obsolete or substandard stocks. The importance of the indicator is connected with the fact that profit occurs with each "turnover" of stocks (ie, use in production, operating cycle).

In most theoretical sources inventory turnover ratio is calculated as the ratio of the cost of production to the average value of stocks for the period, work in progress and finished goods in stock (inventory turnover by value - Oz):

Oz \u003d C / ((Znp + Zkp) / 2)

Where,

C - the cost of products manufactured in the billing period;

Znp, Zkp - the value of the balance of inventories, work in progress and finished products in stock at the beginning and end of the period.

The total cost of goods sold during a given period, usually a year (Cost of goods sold rather than sales is preferred, since the latter includes gross margin, which tends to inflate the turnover rate), divided by the average inventory during the period. of the same period, gives a number showing how many times the product has been turned around.

More visual and convenient for analysis is the inverse indicator - the period of circulation of stocks in days (Pos). It is calculated by the formula:

Pos = Tper / Oz

where, Tper is the duration of the period in days.

The higher the inventory turnover, the more efficient its activities, the less the need for working capital and the more sustainable financial position enterprises, other things being equal.

The calculated periods of turnover of specific components of current assets and current liabilities have a real economic interpretation.

For example, an inventory turnover period of thirty days means that with the production volume prevailing in this analysis period, the enterprise has stocks for 30 days.

Take into account several types of inventory turnover:

- the turnover of each item of goods in quantitative terms (by pieces, by volume, by weight, etc.);

- turnover of each item of goods by value;

- turnover of a set of items or the entire stock in quantitative terms;

- turnover of a set of items or the entire inventory by value.

Evaluation of turnover is an essential element of the analysis of the efficiency with which the company manages inventories. The acceleration of turnover is accompanied by an additional involvement of funds in circulation, and the slowdown is accompanied by the diversion of funds from economic circulation, their relatively longer deadening in stocks (in other words, the immobilization of their own working capital). In addition, it is obvious that the company incurs additional costs for storing inventory, associated not only with storage costs, but also with the risk of damage and obsolescence of goods.

As a result, when managing stocks, stale and slow-moving goods, which are one of the main elements of immobilized (ie, excluded from active economic circulation) working capital, should be subject to special control and revision.

IN Western banking practice analysts usually use an alternative formula - the ratio of inventory to revenue multiplied by 365 days. The formula looks like:

Oz = (Inventory / Net Revenue) x 365

The value of stocks is taken at the end of the period, as it is usually estimated in dynamics. The value of inventories is correlated not with cost, but with revenue as one of the most important factors for credit analysis (thus providing a unified approach to companies that sell goods and services, because for the latter, most of the costs are not for cost, but for general commercial and Administrative expenses). Many people believe that correlation with the cost price gives a more accurate result, since there is a trading margin in the revenue, which artificially increases the turnover, but, on the other hand, the uniformity of the approach is preserved (for example, asset turnover is revenue divided by the amount of assets), in addition, this method is convenient when calculating the operating cycle.

In principle, it is possible that at the beginning of the period and at the end of the period, the stocks are equal to zero. Then the turnover rate can be calculated by taking the average value of stocks in the period (of course, if you have access to this data).

Previously, it was certainly believed that accelerating the turnover of a warehouse is good. Inventory turnover characterizes the mobility of the funds that the company invests in the creation of stocks: the faster the money invested in stocks is returned to the enterprise in the form of proceeds from the sale of finished products, the higher the business activity of the organization. What gives us a more careful consideration of the processes taking place with the warehouse? The turnover itself does not mean anything - you need to track the dynamics of the change in the coefficient, taking into account the following factors:

- the coefficient decreases - the warehouse is overstocked;

- the coefficient is growing or very high (shelf life is less than one day) - work "from the wheels", which leads to failures in the shipment of goods to customers.

In conditions of constant shortages, the average value of the warehouse stock may be equal to zero: for example, if demand is growing all the time, and the company does not have time to bring goods. As a result, there are gaps in the warehouse, there are shortages of goods and unsatisfied demand. If the size of the order decreases, the costs of ordering, transporting and processing goods increase. Turnover increases, but availability problems remain. There are options for a justified increase in inventory - during a period of high inflation or expectations of sharp changes in exchange rates, as well as in anticipation of seasonal peaks in buying activity.

If a company is forced to store in a warehouse goods of irregular demand, goods with a pronounced seasonality, then achieving a high turnover is not an easy task. To ensure customer satisfaction, the company will be forced to have a wide range of infrequently sold products, which will slow down the overall inventory turnover. It is also possible that the supplier provides a good discount (for example, 5-10%) for a significant amount plus a significant deferred payment (in a crisis, such an offer is difficult to refuse).

Also, the terms of delivery of goods play an important role for the store: if the purchase of goods is made using its own funds, then the turnover is very important and indicative. If on credit, then own funds are invested to a lesser extent or not invested at all - then the low turnover of goods is not critical, the main thing is that the loan repayment period does not exceed the turnover indicator. If the goods are taken mainly on the terms of sale, then first of all it is necessary to proceed from the volume of storage facilities and the turnover for such a store is the last indicator in importance.

In fact, it is useful to remember more often that the numbers themselves do not say anything about the effectiveness of inventory management. For example, in retail bread and expensive cognac have completely different indicators - the turnover of bread is many times higher than cognac. It is obvious that bread has one “task” in the store, while cognac has a completely different one and, perhaps, the store earns more from one bottle of cognac than from sales of bread in a week.

Money is the only and universal measure, and by no means kilograms, pieces, cubic meters, etc. Companies invest in a product some amount and want to get the most out of them (return on investment).

inventory turnover shows how many times during the analyzed period the organization used the average available inventory balance.

This indicator characterizes the quality of reserves and the effectiveness of their management, allows you to identify the remains of unused, obsolete or substandard reserves. The importance of the indicator is connected with the fact that profit occurs with each "turnover" of stocks (ie, use in production, operating cycle). Please note that in this case, stocks are understood to mean both commodity stocks (stocks of finished products) and production stocks (stocks of raw materials and materials).

The higher inventory turnover company, the more efficient production is and the less the need for working capital for its organization.

Inventory Turnover Calculator

Online calculator for calculation financial indicator— inventory turnover ratio

Inventory Turnover Formula

Average inventory balance = (Inventory at the beginning of the period + Inventory at the end of the period) / 2

Inventory turnover = Cost of goods sold / Average inventory balance

Inventory Turnover Example

It is necessary to compare the value of the inventory turnover ratio for two enterprises with the following financial results:

- the cost of goods sold of enterprise A was 923 thousand, and enterprise B - 1072 thousand rubles.

- the amount of reserves, respectively, is 429 thousand rubles and 398 thousand.

Calculate the value of the inventory turnover ratio for enterprise A:

ITR a = 923 / 429 = 2,15152.

Calculate the value of the inventory turnover ratio for enterprise B:

ITR b = 1072 / 398 = 2,69347.

Let's compare the values of the coefficients:

ΔITR= ITR b / ITR a

= 1,25278

Enterprise B has a 25.27% higher inventory turnover ratio than Enterprise A.

Popular

- Start in science Net weight of eggs without shell = - - - - - - - - -

- How to delete photos in classmates How to remove tinsel from a photo on classmates

- How to add a photo in a contact?

- Tatyana Gordienko: Other designers copy me and I'm happy about it!

- Personal account Linii Lubvi (Lines of Love)

- Familia: “In retail, the simplest things work best Where can I find the addresses of all department stores in the network

- The most famous low models Parameters of the ideal model

- The technical audit includes

- Technical audit of the enterprise and features of its providence

- Scrap steel construction specifications GOST Scrap steel construction specifications